Why the Opinions of the Bond Rating Agencies Matter

To clear things up, the bond rating agency DBRS did not downgrade the province’s bond rating. It confirmed New Brunswick at A (high) and R-1 (middle) but it changed the trend from stable to negative. This matters because in the fairly arcane world of bond rating agencies every single word has significance.

DBRS concludes that the provincial government’s debt is a little more worrisome because there are no big investment projects on the horizon and there is a shrinking labour market – making the province vulnerable to shocks. Sound familiar?

What does this mean? It’s actually pretty simple. New Brunswick has to issue hundreds of millions of dollars worth of bonds in a typical year (for new debt and to roll over some of the $14 billion in debt that comes due) and if the bond rating agencies get more cranky that will lead to higher interest rates, meaning the cost of servicing the debt will go up – kind of like your personal interest rate if you have a bad credit rating.

Overall, regardless of the bond rating, New Brunswick remains vulnerable to increasing interest rates.

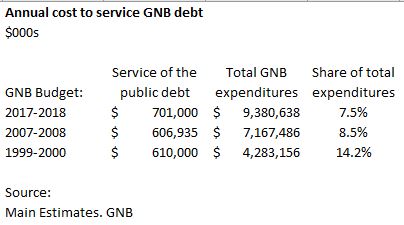

But facts are facts. As shown below we pay a lot less today as a share of the total budget on interest payments (service of the public debt) than we did 15 years ago because of lower interest rates.

David Campbell writes a blog about economic development in Atlantic Canada called It’s The Economy, Stupid. This post was republished with permission. Campbell also operates Jupia Consultants, a consulting company that conducts demographic and economic analysis.

Huddle publishes commentaries from groups and individuals on important business issues facing the Maritimes. These commentaries do not necessarily reflect the opinion of Huddle.