Why The Private Sector Is Responsible For N.B.’s Recent Growth Spurt

New Brunswick’s economy did quite well over the last three years. Politicians being politicians, they love to take credit for this. As Saul Goodman said in Breaking Bad, “people love to take credit for the fun ones.”

But what really accounts for New Brunswick’s recent growth spurt?

To answer this question, it helps to contrast the last three years with the three previous ones.

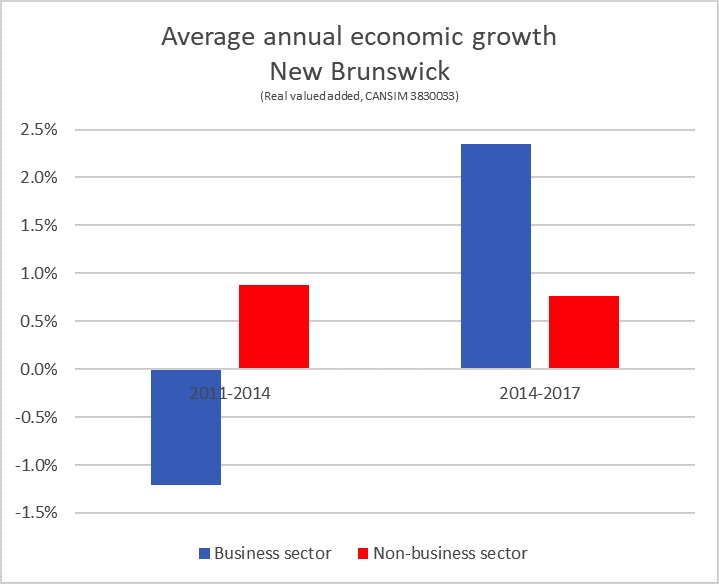

From 2011 to 2014, New Brunswick’s economy declined on average by 0.5 per cent annually. Over the next three years, it grew on average by 1.8 per cent.

As the chart below illustrates, this reversal of fortune is overwhelmingly a business sector story.

Growth in the non-business sector (which includes the government sector – more on this below) was more or less the same throughout.

So, what gave New Brunswick’s business sector such a powerful boost? Was it politicians waving their magic wands or largely factors beyond our control?

I have argued on several occasions that it’s the latter. Among those factors beyond our control were sharp declines in the price of oil and the loonie, as well as a tight North American economy. Let’s go back briefly over each of them.

- In the summer of 2014, oil traded well above $100 U.S. (WTI). Barely six months later, it sold for less than half as much, one of the sharpest drops in history. Such a major decline is a powerful economic stimulant for a non-oil producing province like ours, for two main reasons. First, it leaves more money in the pockets of New Brunswickers, which they can use to buy more stuff locally. Second, as Canada’s economy circa 2014 was behaving much like that of a petro-state, the sharp drop in oil prices led the Bank of Canada to react aggressively to cushion the blow, lowering its policy rate by 50 basis points in the aftermath. Lower rates, as we know, stimulate more borrowing, more purchases, and (in some cases, at least) more investment.

- In turn, lower oil prices and lower interest rates led to a sharp decline in the currency. In the summer of 2014, the loonie traded at around 92-93 cents (U.S.). One year later, it was worth around 76-77 cents, a roughly 20 per cent drop. Of course, a lower loonie means that N.B. exporters are more competitive and get more money for their exports. A lower loonie, however, does not make New Brunswick’s trees grow faster or fish and seafood more abundant; in other words, there are limits to how high the value of N.B.’s exports can grow without further declines in the currency.

- North America’s economy is now very tight, running very close to, or at full potential, depending on which economists you listen to. The U.S. unemployment rate is now below 4 per cent, about half of where it stood five years ago. Similarly, Canada’s unemployment rate, at 5.8 per cent, is at a more than 40-year low. Naturally, a robust North American economy means strong demand for goods and services, including those produced by New Brunswickers.

Still not convinced that Fredericton (or Ottawa excluding the Bank of Canada, for that matter) had little to do with New Brunswick’s recent sugar high? Well then, let’s dig deeper into the numbers.

Below is a list of the industries that have contributed the most to economic growth over the last three years. It is not an exhaustive list (it excludes construction, which we discuss separately below), nor is it a methodologically complete way of telling the growth story over the past three years.

Still, it does give you a pretty good sense of what drove the economy. Combined, the items listed below account for almost all of New Brunswick’s growth over the last three years.*

If what I’ve said above about what drove N.B.’s sugar high is right, then you would expect export-oriented industries to have performed very well over the last three years. This has turned out to be so. As you can see on the chart, heavily export-oriented major industries accounted for the lion’s share of our growth over that period.

Oh, and by the way, this chart actually underestimates the role of exports in fueling our recent growth spurt. Every first-year economics student learns about the so-called “multiplier effect”, which can be summed up as the additional impact of new money injected into the economy.

More exports means more money in New Brunswickers’ pockets, which in turns means more retail sales, such as automobiles, and more financing activity to allow people to purchase those automobiles. Thus, much of the growth in the retail, wholesale, transportation and FIRE sectors that you see above was fueled by the turnaround in export-oriented industries.

Government operations didn’t contribute much to economic growth

Let’s now turn to the contribution of government to New Brunswick’s recent economic sugar high.

You may have noticed from the charts above that I am using “real value added” rather than “gross domestic product” (GDP) to measure economic growth.

This measure makes slight adjustments to GDP data to avoid some double-counting. Without getting bogged down in details, real value added and GDP figures are similar, but real value added is quite useful when it comes to making industry-by-industry comparisons.

StatCan provides a great deal of details on real value-added by industry. Helpfully, it also separates real value added by the business, non-profit and government sectors (the latter two form the “non-business” sector).

Below I discuss two ways government spending can be captured in the data on real value added.

The first is the monetary value of government operations. Here, the contribution of government to growth has been marginal. According to StatCan, real value added in the government sector over the past three years grew by 0.2 percent annually on average.

By contrast, real value added in the business sector grew on average 2.4 percent annually, or 12 times faster than the government sector. It is thus fairly obvious that government operations did not account for much of the province’s recent economic growth.

A second way that governments can influence growth is by funding projects delivered by the private sector. The obvious candidate here is construction activity; after all, governments have been busy doling out money for various infrastructure projects in recent years.

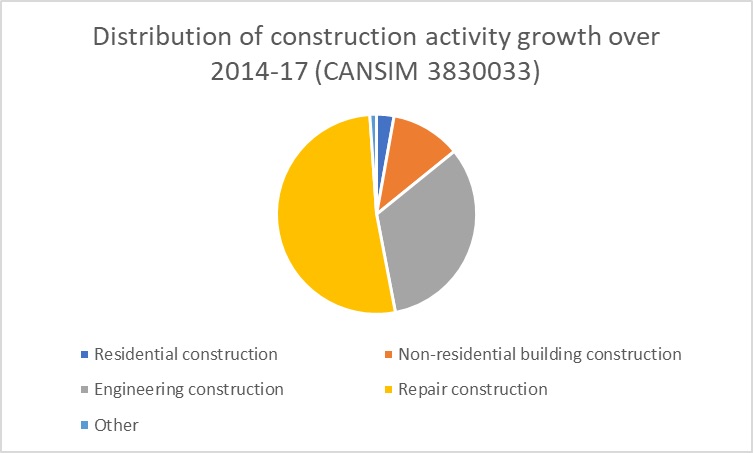

This extra spending does indeed seem to be reflected at least in part in the data, with construction activity in the business sector $156 million higher in 2017 than in 2014. This is not a negligible amount, but the fact remains that it’s more than three times smaller than the contribution of major export-oriented industries.

Here is the breakdown of the $156 million increase in business sector real value added in the construction sector over the past three years.

Of note, residential construction did not change much despite solid economic growth and lower interest rates. This is in no small part because housing activity also depends on population growth and we all know N.B. has not been doing well on that count.

In grey is the so-called “engineering construction” activity: this is where new highway and most other infrastructure projects likely fit in. Real value added in this area was up about $50 million.

Finally, repair construction (in yellow) was where most growth occurred: a bit over $80 million. Although I presume this includes highway maintenance funded but not delivered by the government, it likely also includes major maintenance repairs in the private sector (an example of this could be major maintenance at an oil refinery). Recall that not all construction activity is government-financed (fortunately!)

In short, the role of government in stimulating growth through private sector construction activity was likely quite modest. Indeed, even if we allocated half of the extra construction activity to government-financed infrastructure projects, that would not even amount to one-sixth of what was injected in the economy by major export-oriented industries.

Was it worth adding several hundreds of millions to the public debt to get such a relatively small impact? I’ll let you be the judge.

Sugar highs don’t last forever, nor will N.B.’s recent strong growth spurt.

The reality is that much of what fueled our high is now gone. Oil prices are moving up. The currency remains low, but we saw above that, to have a sustained strong impact on growth, it must keep going down sharply.

This is not what is happening as the loonie remains around where it was three years ago. We’re thus left with a strong North American economic backdrop, but even there, most forecasters are predicting Canada is headed down from last year’s 3 per cent growth rate to slightly below 2 per cent, which is about the rate they believe it can sustain in the long run.

Given its much older and faster-aging population, New Brunswick cannot expect 2 per cent growth in the long run. Most economists, myself included, are of the view that New Brunswick cannot expect much better than 0.5 to 1 per cent growth unless it finds ways to reverse its declining labour force. Incidentally, this is the growth rate that RBC, BMO and others are projecting for New Brunswick this year and next.

Whoever — or, more accurately, whatever — was responsible for New Brunswick’s recent sugar high, the fun part is now mostly behind us.

A more subdued outlook, along with the fact that the oldest baby boomers will turn 75 in three short years, will make balancing the books while providing essential services a much less pleasant experience over the next mandate.

_______________

* Other smaller sectors also made positive contributions, largely offset by those that posted declines.